Below you will find the latest Medicare facts and figures.

2026 Updates to Medicare for You: A Smart Person’s Guide

Medicare Premiums and Costs

UPDATED FACTS: Premiums for Part A, Hospital Insurance, and Part B, Medical Insurance

- Every Medicare beneficiary, regardless of the additional coverage they selected, must pay the Part B premium. In 2026, that is $202.90.

- Those who do not qualify for premium-free Part A and have earned 30 credits will pay $311 a month. Those with fewer than 30 credits will pay $565.

SECTIONS WHERE THIS APPEARS:

- The Parts and Paths of Medicare: The Three Parts of Medicare and Costs Overview

- The Parts and Paths of Medicare: Federal Employees Health Benefits (FEHB) Plans

- Medicare Premiums: Premiums for Medicare Coverage

- Medicare Premiums: Questions and Answers about Medicare Premiums

________________________________________________________

UPDATED FACTS: IRMAA (Income-related Monthly Adjustment Amount)

- For those enrolling in Medicare Part B in 2026, Social Security reviews their 2024 tax records.

- The IRMAA thresholds are as follows: $218,000 for a married individual filing a joint return (both spouses will have to pay any adjustments), $109,000 for a single filer, and $109,000 for a married individual filing a separate return.

SECTION WHERE THIS APPEARS:

• Medicare Premiums: IRMAA

________________________________________________________

Late Enrollment Penalties

UPDATED FACTS: 2026 Part A, Part B, and Part D Penalties

- The Part B late enrollment penalty is 10 percent of the standard Part B premium for every year (a full 12 months) enrollment is delayed. The penalty amount is $20.29 (10 percent of $202.90).

- The Part D late enrollment penalty amount is $0.3899 (1 percent of $38.99) for each month without drug coverage.

- Part A late enrollment penalty amount in 2025 for those who have 30–39 credits is $31.10 and $56.50 for those with fewer than 30 credits.

SECTION WHERE THIS APPEARS:

• Determine Your Timing: Questions and Answers about the IEP

_______________________________________________________________________

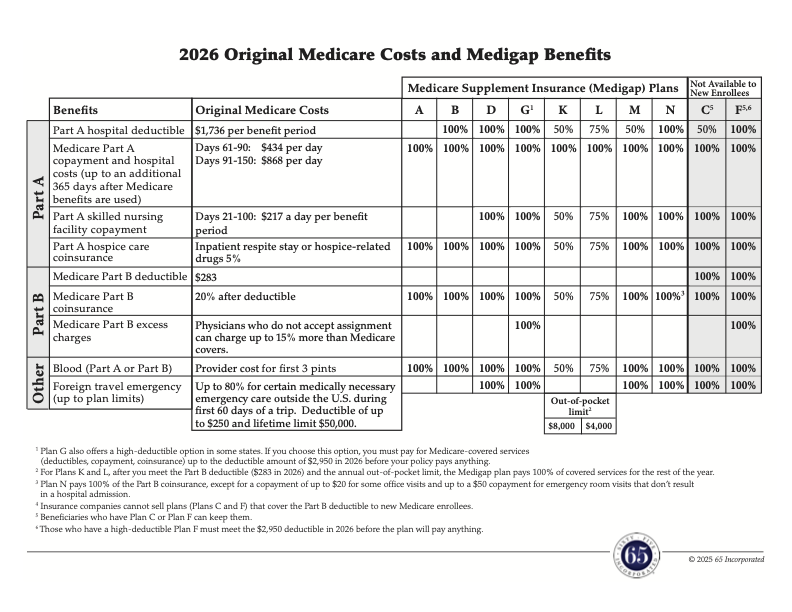

Original Medicare Costs

UPDATED FACTS: Medicare Part A, Hospital Insurance

- The Part A hospital deductible is $1,736 per benefit period.

- The extended hospitalization copayment is $434 for days 61–90 in a benefit period, and $868 per day for days 90–150 (lifetime reserve days).

- The skilled nursing facility (SNF) copayment is $217 for days 21–100.

- The monthly premium for Part A for those who earned at least 30 credits (30 quarters of coverage) is $311. Those who have fewer than 30 credits pay $565.

________________________________________________________

UPDATED FACTS: Medicare Part B, Medical Insurance

The annual Part B deductible is $283, up from $257.

SECTIONS WHERE THIS APPEARS:

- The Parts and Paths of Medicare: Medicare Costs and the Need for Additional Coverage

- Living with Medicare: Part A, Hospital Insurance

- Living with Medicare: Part B, Medical Insurance

- Living with Medicare: Questions and Answers about Part A and Part B Services

________________________________________________________________________

Part D, Prescription Drug Coverage

It is the second year of the Inflation Reduction Act.

UPDATED FACTS: Part D Costs

- The cap on Part D out-of-pocket costs is $2,100, an increase of $100. Remember, this cap applies only to covered medications, those listed in a plan’s formulary that are received from an in-network pharmacy.

- The standard deductible is $615, an increase of $25. Stand-alone and Medicare Advantage plans determine the deductible for their drug coverage and can charge any amount from no deductible, up to $615, the maximum allowed in 2026.

- The base premium is $38.99, compared to $36.78 last year.

- The Part D late enrollment penalty is $0.3899 for every month without creditable prescription drug coverage.

SECTION WHERE THIS APPEARS:

- Living with Medicare: Part D, Prescription Drug Coverage

________________________________________________________

UPDATED FACTS: Medicare Prescription Payment Plan (MPPP)

1. Effective during Open Enrollment in 2025, those who participate in the the MPPP will be reenrolled automatically for the next year.

• The drug plan must send the renewal notice after the end of the annual coordinated election period (Open Enrollment) but prior to the beginning of the plan year (January 1).

• The participant can opt out of the automatic renewal.

• Those who switch drug plans would not be eligible for automatic renewal; they would need to re-enroll if wishing to continue in the MPPP in the new year.

2. A pharmacy does not have to inform the enrollee about the actual out-of-pocket cost of the drug. Instead, CMS “continues to encourage pharmacies to leverage standard industry transaction set data to provide OOP costs to participants verbally upon request.” Because education about the MPPP is the plan’s responsibility, customers may leave the pharmacy without the prescription until they figure out the impact on their monthly payments.

3. If a Part D plan bills an MPPP enrollee over the maximum monthly cap (determined by a formula), it should work with the individual to decide whether to refund the difference or apply the overpayment to the remaining out-of-pocket costs.

Learn more about the Part D cap and MPPP https://www.forbes.com/sites/dianeomdahl/2024/08/08/prepare-for-medicares-first-installment-payment-plan-the-part-d-mppp.

________________________________________________________

UPDATED FACTS: Part D Voluntary Premium Stabilization Demonstration

The demonstration to stabilize monthly premiums for Part D stand-alone plans continued into 2026, with some changes.

- The reduction in the base beneficiary premium (used to calculate the plan-specific basic premium) for all participating stand-alone Part D plans was $10, a decrease of $5 from 2025.

- Premiums increases were limited to $50, up from $35 in 2025.

________________________________________________________

UPDATED FACT: There are two 5-star Part D drug plans, the same number as in 2024 and 2025.

SECTIONS WHERE THIS WOULD APPEAR:

- Living with Medicare: Part D, Prescription Drug Coverage

- Shopping for Coverage: Shopping for Part D, Prescription Drug Coverage

- Medicare Premiums: Premiums for Medicare Coverage

- Other Important Things You Need to Know: Open Enrollment and Changing Plans

____________________________________________________________________________________________________________

Medigap Policies (Medicare Supplement Insurance)

UPDATED FACTS: Medigap Costs

The deductible for high-deductible Plan F and Plan G is $2,950.

SECTION WHERE THIS APPEARS:

- Shopping for Coverage: Shopping for a Medigap Policy

________________________________________________________

UPDATED FACT: Birthday Rules

There are now 12 states with a birthday rule, allowing those who have a Medigap plan to make a change during a period related to their birthday. Those states are California, Idaho, Illinois, Indiana, Kentucky, Louisiana , Maryland, Nevada, Oklahoma,Oregon, Utah, and Virginia.

SECTION WHERE THIS APPEARS:

• Other Important Things You Need to Know: Open Enrollment and Changing Plans

_______________________________________________________________________

Medicare Advantage Plans

UPDATED FACTS: Medicare Advantage Plans

- The maximum out-of-pocket limit in 2026 is $9,250 for in-network care and $13,000.

- There are 18 Medicare Advantage plans that earned a 5-star rating.

- On the other end of the spectrum, four Advantage plans received a low performing icon for consistently low-quality ratings.

SECTIONS WHERE THIS APPEARS:

- The Parts and Paths of Medicare: The Three Parts of Medicare and Costs Overview

- Shopping for Coverage: Shopping for a Medicare Advantage Plan

- Living with Medicare: Questions and Answers about Your Medicare Path

____________________________________________

UPDATED FACT: Member Notification of Unused Benefits

The Centers for Medicare and Medicaid Services was going to require Medicare Advantage plans to issue an annual “Mid-Year Enrollee Notification of Unused Supplemental Benefits,” between June 30 and July 31, 2026. However, in September 2025, CMS announced a“temporary enforcement pause” of the requirement. CMS took the action because the plans had a “barrage of questions and requests for technical guidance.”

SECTION WHERE THIS WOULD APPEAR:

• Shopping for Coverage: Shopping for a Medicare Advantage Plan

_______________________________________________________________________

New in 2026

The WISeR Model

WISeR stands for Wasteful and Inappropriate Service Reduction, another creative acronym from CMS. An Innovation Center model is testing a new process to determine whether enhanced technologies, including artificial intelligence (AI), can expedite the prior authorization processes.

Here are some things to know.

• The test will run for six years, from January 1, 2026, to December 31, 2031, in six states – Arizona, New Jersey, Ohio, Oklahoma, Texas, and Washington.

• There are 17 items and services on the list that will require prior authorization for Original Medicare beneficiaries.

• The model is voluntary. If a provider does not submit a request, the claim will be subject to the usual pre-payment review.

• There are 17 items and services on the list that will require prior authorization. (Find the list on page 7 of the Federal Register notice athttps://public-inspection.federalregister.gov/2025-12195.pdf.)

• WISeR will apply only to Original Medicare. (CMS published a separate final rule for Medicare Advantage prior authorization. However, that rule focuses on standardizing and streamlining processes and communication. It does not target a specific group of services.)

• Medicare wants to reduce fraud, abuse, and waste, including low-value care and believes the 17 services are related to that.

For more information, check www.forbes.com/sites/dianeomdahl/2025/07/22/medicare-prior-authorization-getting-wiser-five-essential-questions and www.cms.gov/priorities/innovation/innovation-models/wiser.

SECTION WHERE THIS WOULD APPEAR:

• The Parts and Paths of Medicare: The Two Medicare Paths

________________________________________________________________________

Check this page for more updates as they become available.

2025 Updates to Medicare for You: A Smart Person’s Guide

Original Medicare Costs

UPDATED FACT: The Part B deductible is $257.

SECTIONS WHERE IT APPEARS:

- Shopping for Coverage: Questions and Answers about a Medicare Advantage Plan

- Shopping for Coverage: Questions and Answers about a Medigap Policy

- Living with Medicare: Part B, Medical Insurance

UPDATED FACT: The Part A hospital deductible is $1,676 per benefit period.

SECTIONS WHERE IT APPEARS IN THE BOOK:

- The Parts and Paths of Medicare: Medicare Costs and the Need for Additional Coverage

- Living with Medicare: Part A, Hospital Insurance

- Living with Medicare: Questions and Answers about Part A and Part B Services

UPDATED FACT: Extended hospitalization copayment is $419 for days 61–90 in a benefit period, and $838 per day for days 90–150 (lifetime reserve days).

SECTIONS WHERE IT APPEARS:

- The Parts and Paths of Medicare: Medicare Costs and the Need for Additional Coverage

- Living with Medicare: Part A, Hospital Insurance

- Living with Medicare: Questions and Answers about Part A and Part B Services

UPDATED FACT: The skilled nursing facility (SNF) copayment is $209.50 for days 21–100.

SECTIONS WHERE IT APPEARS:

- The Parts and Paths of Medicare: Medicare Costs and the Need for Additional Coverage

- Living with Medicare: Part A, Hospital Insurance

Part D, Prescription Drug Coverage

The Inflation Reduction Act has changed many things about Part D prescription drug coverage. It’s as though Part D coverage has been put into a blender and we have to figure out the new concoctions.

UPDATED FACTS:

In 2025, the donut hole, officially called the Coverage Gap, is gone and there is a cap on Part D out-of-pocket costs. No one will pay more than $2,000.

These are some important points.

• It applies only to covered medications, those listed in a plan’s formulary.

• The cap does not include monthly premiums or Part B and noncovered drugs.

• It will be indexed annually for inflation.

• There is no need to sign up for this limit; it will apply automatically.

Find more information about the $2,000 cap at https://www.forbes.com/sites/dianeomdahl/2024/08/01/good-bye-medicare-part-d-donut-hole-hello-2000-cap/.

With the donut hole gone, there are three payment stages.

1. The standard deductible will be $590.

2. Initial Coverage remains the second step. The threshold to enter the next stage is $2,000.

3. Catastrophic Coverage is the last payment stage and there are no costs for medications.

The $2,000 cap spawned a new program: the Medicare Payment Prescription Plan. This resembles an installment payment plan. Those who reach the cap in the first month or two of the year will face a big bill at the pharmacy. This new plan allows a drug plan member to spread out the costs over the year, instead of all at once.

Here is what you should know about this program.

• Anyone who has Part D drug coverage is eligible for this program.

• Those who want to participate in this program must enroll.

• The plan applies only to Part D medications listed in a plan’s formulary and from an in-network pharmacy.

• The member pays the drug plan, not the pharmacy.

• The amount of the monthly bills can vary.

Learn more about this program at https://www.forbes.com/sites/dianeomdahl/2024/08/08/prepare-for-medicares-first-installment-payment-plan-the-part-d-mppp.

It’s also important to know that not everyone will benefit from this plan. Find some examples at https://www.forbes.com/sites/dianeomdahl/2024/11/20/the-medicare-prescription-payment-plan-yay-or-nay/.

SECTION WHERE THEY APPEAR:

- Living with Medicare: Part D, Prescription Drug Coverage

UPDATED FACT: There are two 5-star Part D drug plans, the same number as in 2024.

SECTION WHERE IT APPEARS:

Shopping for Coverage: Prescription Drug Coverage

Other Important Things You Need to Know: Open Enrollment and Changing Plans

Medigap Policies (Medicare Supplement Insurance)

UPDATED FACT: The deductible for high-deductible Plan G is $2,870.

SECTION WHERE THEY APPEAR:

- Shopping for Coverage: Shopping for a Medigap Policy

UPDATED FACT: There are now eight states–California, Idaho, Illinois, Kentucky, Louisiana , Maryland, Nevada, Oklahoma, and Oregon–with a birthday rule, allowing those who have a Medigap plan to make a change during a period related to their birthday.

SECTION WHERE IT APPEARS:

- Other Important Things You Need to Know: Open Enrollment and Changing Plans

Medicare Advantage Plans

UPDATED FACT: The maximum out-of-pocket limit in 2024 is $9,350 for in-network care and $14,000.

SECTIONS WHERE IT APPEARS:

- The Parts and Paths of Medicare: The Three Parts of Medicare and Costs Overview

- The Parts and Paths of Medicare: Questions and Answers about the Medicare Paths

- The Parts and Paths of Medicare: Questions and Answers about Your Medicare Path Decision

- Living with Medicare: Questions and Answers about Your Medicare Path

UPDATED FACTS:

The quality of plans is declining.

• In 2025, there are only seven 5-star Medicare Advantage plans, down from 74 in 2022.

• On the other end of the spectrum, the number of Advantage plans receiving 2 or 2.5 stars increased from two in 2022 to 24 in 2025.

SECTIONS WHERE THEY APPEAR:

- Questions and Answers about Part D Prescription Drug Coverage

- Shopping for Coverage: Shopping for a Medicare Advantage Plan

- Other Important Things You Need to Know: Open Enrollment and Changing Plans

Medicare Premiums

UPDATED FACT: The Part B premium is $185.

SECTIONS WHERE IT APPEARS:

- The Parts and Paths of Medicare: The Three Parts of Medicare and Costs Overview

- The Parts and Paths of Medicare: Federal Employees Health Benefits (FEHB) Plans

- Medicare Premiums: Premiums for Medicare Coverage

- Medicare Premiums: Questions and Answers about Medicare Premiums

UPDATED FACT: Those who do not qualify for premium-free Part A and have earned 30 credits will pay $285 a month. Those with fewer than 30 credits will pay $518.

SECTION WHERE IT APPEARS:

- Medicare Premiums: Premiums for Medicare Coverage

UPDATED FACT: The premiums for stand-alone Part D drug plans start as low as $0.00 in a few areas and go up to $200 or more.

SECTION WHERE IT APPEARS:

- Living with Medicare: Part D, Prescription Drug Coverage

IRMAA (Income-related Monthly Adjustment Amount)

UPDATED FACTS:

- For those enrolling in Medicare Part B in 2025, Social Security reviews their 2023 tax records.

- The IRMAA thresholds are as follows: $206,000 for a married individual filing a joint return (both spouses will have to pay any adjustments), $103,000 for a single filer, and $103,000 for a married individual filing a separate return.

SECTION WHERE THEY APPEAR:

- Medicare Premiums: IRMAA

Late Enrollment Penalties

UPDATED FACTS:

- The Part B late enrollment penalty is 10 percent of the standard Part B premium for every year (a full 12 months) enrollment is delayed. In 2025, the penalty amount is $18.50 (10 percent of $185). Three years late enrolling in Part B adds $55.50 to the monthly premium.

- The Part D late enrollment penalty amount is $0.3678 (1 percent of $36.78) for each month without drug coverage.

- Part A late enrollment penalty amount in 2025 for those who have 30–39 credits is $28.50 and $51.80 for those with fewer than 30 credits.

SECTION WHERE IT APPEARS:

- Determine Your Timing: Questions and Answers about the IEP

New in 2025

Here is a list of more significant changes for 2025.

Part B Inflation Rebates

The Inflation Reduction Act requires drug companies to pay a rebate if they raise their prices for certain drugs faster than the rate of inflation. These rebates will go into the Medicare Trust Fund. Beneficiaries will pay 20% of the inflation-adjusted payment amount, which will be less than what they would pay in coinsurance otherwise.

Drug Price Negotiation

Medicare can now negotiate directly with manufacturers on Part B and Part D drugs. Experts expect the negotiations will save Medicare $164 billion over 10 years, lowering the amount that Medicare spends for drugs.

The first round of negotiated prices will take effect in January 2026. The ten drugs are among the highest annual Part D spending and include Eliquis, Enbrel, Jardiance, Novolog, Stelara, and Xarelto.

Beneficiaries may or may not see savings for several reasons.

• Many of the drugs are going off patent and cheaper generics will be available.

• There is competition between similar branded medications.

• Insulin is already capped at $35.

Plans won’t be required to cover similar ones so some could lose access to medications they currently take.

Medicare Advantage Supplemental Benefits Notification

In 2022, over 99% of Medicare Advantage plans offered at least one supplemental benefit. The median was 23 supplemental benefits, and the most frequently offered benefits were vision, hearing, fitness, and dental. Some plans have indicated that enrollee utilization of many supplemental benefits is low and Medicare is concerned about the low utilization.

Beginning in 2025, plans must issue an annual “Mid-Year Enrollee Notification of Unused Supplemental Benefits,” between June 30 and July 31, that is personalized to each enrollee. It must include:

• A list of any supplemental benefits not accessed by the individual during the first six months of the year

• The scope of the benefit, cost-sharing, instructions on how to access the benefit, and any network application information for each available benefit, and

• A customer service number to call if additional help is needed.

Previous Updates to Medicare for You: A Smart Person’s Guide

Part D Drug Coverage

Insulin

All insulins covered under a Part D plan, whether injected or administered by pump, are now capped at $35. Note this important point: CMS defines “covered” as an insulin that is included on a Part D sponsor’s formulary, the list of drugs it covers. Plans can determine the drugs they cover and can change their formularies.

This rule has created with issues with insulin coverage. 65 Incorporated found that half of the 2025 drug plans don’t cover five to eight of commonly prescribed insulins. Medicare beneficiaries with diabetes should check during the Open Enrollment Period that their Part D plans will cover their insulin each and every year.

Read more about this at https://www.forbes.com/sites/dianeomdahl/2024/10/17/insulin-coverage-what-medicare-beneficiaries-need-to-know-for-2025.

SECTIONS WHERE THIS WOULD APPEAR:

Living with Medicare: Part B, Medical Insurance

Living with Medicare: Part D, Prescription Drug Coverage

Part D Vaccinations

Part B covers many vaccines, such as those for the flu, pneumonia, and COVID, to name a few, with no cost to the beneficiary.

Now, Part D vaccinations are treated just like Part B vaccines. They are not subject to a plan’s deductible and there is no copayment.

These include the following:

• shingles (known as Shingrix)

• hepatitis B administered to non-high-risk individuals

• DTaP (diphtheria, tetanus, pertussis), and

• RSV (respiratory syncytial virus).

Getting Part D vaccinations in a physician’s office can create problems, no matter the Medicare path you chose. To avoid issues, visit a pharmacy that is in the drug plan’s network. Many pharmacies will allow you to schedule an appointment for your visit.

SECTIONS WHERE THIS WOULD APPEAR:

Living with Medicare: Part D, Prescription Drug Coverage

Living with Medicare: Questions and Answers about Part D Drug Coverage

Catastrophic Coverage

With the elimination of the Coverage Gap (donut hole), Catastrophic Coverage is now the third payment stage in a Part D drug plan. Those who have total drugs costs of $2,000 will reach this stage and not pay another penny for the remainder of the year. That means Part D drug plans will now have to pay considerably more, which has caused some ripple effects.

• Many plans increased the copayments for Tier 1 and Tier 2 drugs.

• Some changed a Tier 3 copayment to a coinsurance.

• Plans are increasing the coinsurance for Tier 4 and Tier 5 drugs.

• Premiums have also increased.

Read about this at https://www.forbes.com/sites/dianeomdahl/2023/10/03/medicare-part-d-drug-coverage-in-2024-some-will-pay-less-but-will-others-pay-more/.

SECTION WHERE THIS WOULD APPEAR:

Living with Medicare: Part D, Prescription Drug Coverage

Premium Stabilization

As of January 1, 2024, the premium stabilization initiative in the Inflation Reduction Act limited the Part D base beneficiary premium to a six percent increase over the previous year. But in 2024 plans, there were premiums increases of 25 percent, 39 percent, even 75 percent. So, what’s going on?

The base premium is a starting point for calculating plan-specific basic Part D premiums and the basis of the Part D late enrollment penalty calculations. It is not the one a beneficiary will pay and that is why premiums vary considerably and can increase more than six percent.

CMS was concerned that significant increases in premiums for stand-alone Part D plans could lead enrollees to switch to Medicare Advantage plans. (The average monthly plan premium is $18.50, while many plans have no premium.) In response, CMS instituted a voluntary premium stabilization demonstration that consists of three elements.

1. CMS applied a $15 reduction to the base beneficiary premium (used to calculate the plan-specific basic premium) for all participating stand-alone Part D plans. (Plan premiums cannot drop below $0.)

2. CMS limited premium increases to $35 from 2024 (after the application of the $15 reduction).

3. There will be a change to provide for greater government risk sharing for potential plan losses.

As a result of this demonstration, many premiums went up exactly $35. There was also much fluctuation in premiums. We have no idea what this will mean going forward but we know one thing. Paying attention during the fall Open Enrollment Period will be more important than ever.

Check these links for more information: https://www.forbes.com/sites/dianeomdahl/2023/11/07/are-medicare-part-d-drug-plan-premiums-falling-were-skeptical/ and https://www.forbes.com/sites/dianeomdahl/2024/10/01/2025-drug-plan-premiums-under-control-but-in-flux.

SECTIONS WHERE THIS WOULD APPEAR:

Living with Medicare: Part D, Prescription Drug Coverage

Shopping for Coverage: Shopping for Part D, Prescription Drug Coverage

Nursing Home Residents

Those in a nursing home have opportunities to switch Medicare drug coverage outside regular enrollment periods. Specifically, they can change drug plans:

• upon admission to a nursing home

• once a month while living in the nursing home, and

• during the two months after discharge from the facility

SECTION WHERE IT SHOULD APPEAR:

Other Important Things You Need to Know: Open Enrollment and Changing Plans

Medigap Policies (Medicare Supplement Insurance)

Medigap policies in 47 states are standardized by 10 letters. Each letter represents a package of benefits and costs. Massachusetts, Minnesota, and Wisconsin have their own models, but the policies work the same way.

SECTION WHERE IT APPEARS:

The Paths and Parts of Medicare: Original Medicare Path

Medicare Advantage Plans

PPO Plans and Prior Authorization

As with just about every Medicare Advantage plan, a preferred provider organization (PPO) plan can require healthcare providers to obtain advance approval for any service. However, PPO plans cannot mandate this for out-of-network providers.

No prior authorization may sound amazing but it really isn’t. Most plans will suggest that you ask for a pre-visit coverage decision to confirm that the out-of-network services you’re getting are covered and are medically necessary. This is important because, without this decision, the plan may determine (after the fact) the services were not covered or were not medically necessary. If that happens, you end up with the bill.

Here’s how to avoid those retroactive denials.

• Whenever possible, get necessary medical care from an in-network provider. Prior authorization is generally the provider’s responsibility.

• Examine your plan’s Evidence of Coverage (EOC) for information about prior authorization for out-of-network services.

• Ask a plan representative how to obtain a pre-visit coverage decision if you’re about to receive services from an out-of-network provider.

• File an appeal if your plan determines it won’t cover the care.

SECTION WHERE IT APPEARS:

The Parts and Paths of Medicare: Making Your Medicare Path Decision

Health Systems Dropping Medicare Advantage Plans

In fall 2024, Becker’s Hospital Review reported that 32 health systems across the country are discontinuing their Medicare Advantage contracts. The key issues driving these decisions include low reimbursement rates and/or delays in getting paid, prior authorization denial rates, and administrative costs to manage out-of-network care. The number of contracts being dropped ranges from just one to many. For instance, over 30,000 Medicare Advantage plan members had to scramble to find new health care providers when their specialty health system dropped Medicare Advantage. Those who have been enrolled in Part B for more than six months no longer have a guaranteed issue right and, in most states, would likely need to pass medical underwriting to get a Medigap policy.

No one knows whether more health systems will join this trend or if it will fade away, but this is a factor to consider when making your path decision.

This issue does not have an impact on those who choose the Original Medicare Path.

SECTION WHERE THIS WOULD APPEAR:

The Parts and Paths of Medicare: Making Your Medicare Path Decision

Medicare Advantage Marketing

A law that took effect in 2022 requires insurance agents, brokers, and other third-party marketing organizations (like the ones that sponsor TV ads) to record all calls with beneficiaries in their entirety, including the enrollment process. They must disclose that their information will go to an agent for future contact and they may be transferred to an agent who can enroll them in a plan.

As of January 1, 2023, the Centers for Medicare and Medicaid Services must approve all television ads in advance and review ads already on air to ensure they meet all marketing requirements. During the 2024 Open Enrollment Period, there were very few commercials and those were related to specific plans.

SECTION WHERE THIS WOULD APPEAR:

The Parts And Paths Of Medicare: Medicare Advantage Commercials

Medical Savings Account Plans

The maximum deductible for MSA plans in 2025 is $16,350.

However, according to Q1Medicare.com, there is only one MSA plan left in the country and that is in Wisconsin. The deductible for that plan is $4,600.

SECTION WHERE IT APPEARS:

Shopping for Coverage: Shopping for a Medicare Advantage Plan

Retiree Plans

Since the publication of this book, retiree coverage has undergone many changes. Here’s an overview of today’s situation.

Fewer than 15 percent of large employers offer retiree coverage. The plans may come with discounted premiums or cost sharing and benefits not available to the public. In many cases, the retirees have earned this coverage, may be vested, or have a fund of money, possibly from unused sick days or subsidies, to apply toward the costs.

As previously discussed, retirees must enroll in Part A and Part B during their IEP or SEP. How the retiree group health coverage coordinates with Medicare depends on the terms of the specific plan. For years, retiree plans served as the secondary payer to Medicare, covering costs such as the hospital deductible and 20 percent Part B coinsurance. Retirees had their choice of any physicians who saw Medicare patients.

But recently, Medicare Advantage has taken over. Half of the companies offering retiree coverage do it through Medicare Advantage plans. Employers can save money, primarily because they receive federal payments. With retiree coverage, the plan sponsor controls the coverage and can change the structure, costs, or whatever else. What if the group coverage no longer works for the retiree? Perhaps the plan’s network limits the ability to choose physicians, prior authorization rules delay necessary care, or customer service never answers the phone. These problems can lead to buyers’ remorse. Unhappy retirees could opt out of the coverage and choose a Medicare option available to the public, either a Medicare Advantage plan or a Medigap policy (Medicare supplement plan) and Part D drug plan. However, those who had been enrolled in Part B for more than six months no longer have a guaranteed issue right to get a Medigap policy. They would likely need to pass medical underwriting to purchase a policy.

If that happens, the retiree’s options to change coverage depend on the situation.

SECTION WHERE IT APPEARS:

The Parts and Paths of Medicare: Know When You Need More Help

Medicare Enrollment and Coverage

Dental Services

Medicare now covers the following medically necessary dental services:

• diagnostic and treatment services for infection prior to or with any organ transplant

• reduction of jaw fractures

• oral health services in head and neck cancers, and

• ancillary services incident to these covered services, such as dental x-rays and operating room use.

SECTION WHERE THIS WOULD APPEAR:

Living with Medicare: Other Coverage Concerns

Hearing Exams and Hearing Aids

Over-the counter hearing aids are now available as a cost-effective alternative. No prescription is needed.

SECTION WHERE THIS WOULD APPEAR:

Living with Medicare: Other Coverage Concerns

Telehealth

The Full-Year Continuing Appropriations and Extensions Act extended access to most telehealth benefits for all Medicare beneficiaries until September 30, 2025.

SECTION WHERE THIS WOULD APPEAR:

Living with Medicare: Part B, Medical Insurance

Cologard™

Medicare Part B covers this screening test once every three years for those who show no signs or symptoms of colorectal disease and have no significant, repeated personal or family history.

Discuss any concerns with your physician.

SECTION WHERE THIS WOULD APPEAR:

Living with Medicare: Questions about Part A and Part B Services

Part B Special Enrollment Period for Special Circumstances

Missing the chance to enroll in Medicare can be devastating. Until recently, those who did not enroll on time had little recourse, but things are beginning to change. Medicare now provides a Part B special enrollment period for exceptional circumstances, which include:

• misinformation from an employer

• an emergency or natural disaster

• a release from a correctional facility termination of Medicaid eligibility, and

• other exceptional circumstances.

Remember to document all the details.

SECTION WHERE THIS WOULD APPEAR:

Get Ready for Medicare: Tips to Help You Get Ready

United States Postal Service (USPS) Employees and Annuitants

USPS employees, annuitants, and eligible family members have had Federal Employee Health Benefits (FEHB) plans but, as of January 1, 2025, that changed. The new Postal Service Health Benefits (PSHB) Program is now sponsoring their plans. Eligible individuals had to select a new PSHB plan during the 2024 open season.

Part B enrollment is now a concern.

• If you are an annuitant as of January 1, 2025, and not currently enrolled in Part B, you do not need to enroll to continue with new PSHB coverage. (There was a special enrollment period, ending September 30, 2024, that would have allowed these annuitants to enroll in Part B without penalty.)

• If you are an annuitant enrolled in Part B, you must maintain enrollment to qualify for the PSHB program.

• If you are an active employee under the age of 64 as of January 1, 2025, you will be required to enroll in Part B after retirement and when eligible for Medicare.

Bookmark www.opm.gov/healthcare- insurance/pshb, a good site for updates.

SECTIONS WHERE THIS WOULD APPEAR:

Determine Your Timing: Keeping Employer Group Coverage Past Age 65

The Parts and Paths of Medicare: Know When You Need More Help

Initial Enrollment Period

The IEP, seven months surrounding your 65th birthday, is a time to pay attention to Medicare.

Once you turn 64, use one of these worksheets in the appendix to identify your IEP. Then, during this time, study your situation and determine what, if anything, you need to do about Medicare.

SECTION WHERE IT APPEARS :

Appendix: Initial Enrollment Period (IEP) Worksheets

Websites

Medicaid eligibility: https://www.medicare-links.com/apply-for-medicaid

Marketplace plans: https://www.medicare-links.com/marketplace-plans

Medicare

Help with drug costs: https://www.medicare-links.com/help-with-drug-costs

Medical suppliers directory: https://www.medicare-links.com/medical-supplier-directory

Medicare.gov account: https://www.medicare-links.com/create-a-mymedicare-account

Medicare Savings Programs: https://https://www.medicare-links.com/medicare-savings-program

Personal representative: https://www.medicare.gov/medicareonlineforms/publicforms/cms10106.pdf

Plan Finder: https://www.medicare-links.com/medicare-plan-finder

Plan Finder instructional video: https://www.medicare-links.com/using-the-medicare-plan-finder-video

Physician Compare database: https://www.medicare-links.com/physician-compare

Preventive and screening services: https://www.medicare-links.com/medicares-preventive-services

Medicare appeals

Basics: https://www.medicare-links.com/medicare-interactive-appeal-basics

File appeal: https://www.medicare-links.com/file-a-medicare-appeal

Request for Reconsideration (SSA-561-U2): https://www.medicare-links.com/request-for-reconsideration-form

Medicare costs and premiums

Income-Related Monthly Adjustment Amount—Life-Changing Event (SSA-44): https://www.medicare-links.com/life-changing-event-form

Medicare Easy Pay Premium Statement (CMS-20143): https://www.medicare-links.com/medicare-easy-pay-statement

Medicare Premium Bill: https://www.medicare-links.com/medicare-premium-bill

Patient’s Request for Medical Payment: https://www.medicare-links.com/patients-request-for-medical-payment

Medicare enrollment

Application for Enrollment in Medicare Part B (Medical Insurance) (CMS-40B): https://www.medicare-links.com/enrollment-in-medicare-part-b-application

Checklist for online enrollment: https://www.medicare-links.com/online-enrollment-checklist

Enrollment: https://www.medicare-links.com/social-security-applicatiion

Request for Employment Information (CMS-L564): https://www.medicare-links.com/request-for-employment-information

Medigap policies (Medicare Supplement insurance)

Medigap policies: https://www.medicare.gov/health-drug-plans/medigap

Massachusetts: https://www.medicare-links.com/massachusetts-medigap-policies

Minnesota: https://www.medicare-links.com/minnesota-medigap-policies

Wisconsin: https://www.medicare-links.com/wisconsin-medigap-policies

Postal Service Health Benefits (PSHB) plans: https://www.opm.gov/healthcare-insurance/pshb

Social Security

Home page: https://www.ssa.gov

my Social Security account: https://www.ssa.gov/myaccount

Office locator: https://www.medicare-links.com/find-ssa-office

SHIP counselors: https://www.medicare-links.com/find-ship-counselor

Travelers’ advice: https://www.medicare-links.com/cdc-resources-for-travelers